LIC Cancer Cover Plan 905 | LIC Cancer Cover Plan 905 Premium Calculator | LIC Plan 905 Tax Benefits | LIC Cancer Cover Plan 905 Agent Commission

On November 14th, 2017, LIC has launched a new health insurance plan named LIC Cancer Cover (Plan 905). This is the company’s second health insurance product. This is a kind of regular premium payment health insurance plan. Let’s take a look at its features, benefits, and a review in this article.

LIC is now offering disease-specific health insurance. This is referred to as LIC Cancer Cover (Plan 905). This is a traditional (non-linked) health insurance plan that pays a defined benefit if the Life Assured is diagnosed with any of the specified stages of cancer during the policy period (however, subject to certain terms and conditions).

Table of Contents

LIC Cancer Cover Eligibility (Plan 905)

Let’s start with the eligibility requirements for purchasing this product.

Eligibility for LIC Cancer Cover (Plan 905)

| Feature | Minimum | Maximum |

| Entry Age | 20 years | 65 Years |

| Policy Term | 10 years | 30 Years |

| Cover Ceasing Age | 50 years | 75 Years |

| Basic Sum Assured | Rs 10,00,000 | Rs 50,00,000 |

You’ve probably observed that the highest coverage is merely Rs.50, 00,000. In addition, the maximum age for entry is 65 years old.

This plan is available for purchase ONLINE. According to Section 38 of the Insurance Act of 1983, a policy can be allocated.

LIC Cancer Cover Options (Plan 905)

There are two sorts of Sum Assured options available with this product. In addition, your premium varies depending on the plan you select. You must select this option when purchasing this plan.

Option I – Level Sum Insured

Throughout the policy period, the Basic Sum Insured will stay the same. As a result, the premium will remain constant during the policy term.

Option II – Increasing Sum Insured

Starting from the first policy anniversary or until the diagnosis of the first cancer event, the Sum Insured increases by 10% of the Basic Sum Insured each year for the first five years (whichever is earlier). All claims payable upon diagnosis of any specified cancer will be based on the Increased Sum Insured at the policy anniversary coinciding or before the diagnosis of the first claim, and no additional increases to this Sum Insured will be allowed.

As a result, if you select the second option, your premium will not be consistent throughout the policy time.

Advantages of LIC Cancer Insurance (Plan 905)

The LIC Cancer Cover (Plan 905) rewards are separated into two levels. Keep in mind that this is a disease-specific guide. As a result, you will only be eligible for payments if in case you get will be diagnosed with CANCER during the policy period.

There is no maturity advantage, no surrender value, and no loan facility. There are two types of benefit classifications.

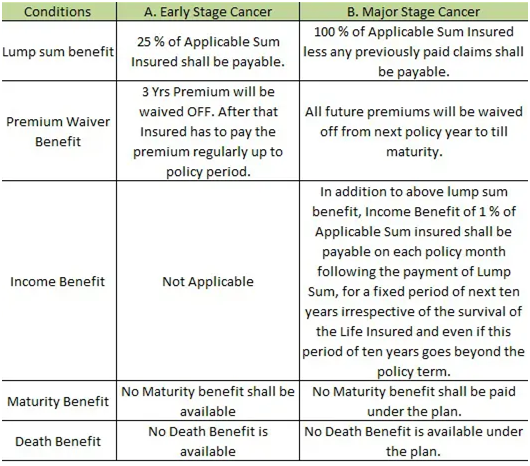

1. Early Stage Cancer

The following benefits are awarded upon the first diagnosis of any of the designated Early Stage Cancers, assuming that the diagnosis is admissible.

- A lump-sum benefit of 25% of the Applicable Sum Insured will be paid.

- Premium Waiver Benefit– From the policy anniversary coinciding or following the date of diagnosis, premiums for the next three policy years or the balance of the policy term, whichever is lower, will be waived.

- After three years of premium waiver, the insured must pay the premium on a regular basis for the remainder of the insurance period.

The Early Stage Cancer Benefit will only be paid once for the first-ever event, and Life Assured will not be able to file another claim for the same or any other cancer. However, the insurance coverage for Major Stage Cancer will remain until the policy expires.

2. Cancer in Advanced Stage

- Lump Sum-100 percent of the Applicable Sum Insured less any previously paid claims in respect of Early Stage Cancer shall be payable on the first diagnosis of the specified Major Stage Cancer, provided the same is acceptable.

- Income Benefit-In addition to the lump sum benefit described above, an Income Benefit of 1% of the Applicable Sum Insured will be paid on each policy month following the payment of the Lump Sum for a fixed period of ten years, regardless of the Life Insured’s survival and even if the ten-year period extends beyond the policy term. The residual payouts, if any, will be paid to the Life Assured’s nominee if the Life Assured dies while receiving this Income Benefit.

- Premium Waiver Benefit-From the following policy anniversary, all future premiums will be waived, and the policy will be free of all liabilities excluding the extension of Income Benefit as indicated above.

No payment for any subsequent claims under Early Stage Cancer or Major Stage Cancer would be acceptable once a Major Stage Cancer Benefit has been paid.

If the life assured makes claims for different stages of same cancer at the same period, the benefit will only be paid for the higher claim that is admitted under the policy.

The Corporation will only pay one benefit if more than one Cancer is detected in an event. The amount pertaining to the stage of cancer with the highest benefit amount will be that benefit.

Plan 905 Benefits Explained

LIC Cancer Cover Tax Advantages (Plan 905)

The premium you pay for this plan is tax-deductible up to Rs.55, 000 per year under Section 80D. Keep in mind that you won’t be able to collect the benefits of premiums paid under Section 80C.

LIC Cancer Cover Premium Review

Only up to 5 years will the premium calculation stay unchanged. Premiums may fluctuate after 5 years based on LIC’s claim experience, but if they do, they will remain unchanged for the next 5 years. (Any premium increase will be computed based on the proposer’s age at the time the insurance is started.)

Definitions of Cancers Covered by Plan 905

Cancer in its Early Stages

Any of the disorders described below must be diagnosed using histological evidence and validated by a professional in the relevant field.

# Carcinoma-in-situ (CIS)

Carcinoma-in-situ refers to the existence of malignant cancer cells that have not spread outside of the cell group from which they originated. It must involve the entire epithelial thickness, but it does not cross basement membranes or invade neighboring tissue or organs. The diagnosis of which requires a microscopic study of fixed tissues to be confirmed.

# Prostate Cancer–early stage

Early Prostate Cancer is histologically described using the TNM classification as T1N0M0 with a Gleason Score 2 (two) to 6 (six).

# Thyroid Cancer – early stage

All thyroid cancers that are less than 2.0 cm and histologically classified as T1N0M0 according to TNM classification.

# Bladder Cancer – early stage

All tumors of the urinary bladder are histologically classified as TaN0M0 according to TNM classification.

# Chronic lymphocytic Leukaemia – early stage

Chronic Lymphocytic Leukaemia is categorized as stage 0(zero) to 2 (two) as per the Rai classification.

# Cervical Intraepithelial Neoplasia

Severe Cervical Dysplasia was reported as Cervical Intraepithelial Neoplasia 3 (CIN3) on cone biopsy.

Major Stage Cancer

A malignant tumor characterized by uncontrolled development and dissemination of malignant cells, as well as invasion and destruction of normal tissues, is a major stage cancer. This diagnosis must be backed up by histological evidence of malignancy. Leukemia, lymphoma, and sarcoma are all types of cancer.

Exclusions for LIC Cancer Cover (Plan 905)

Exclusions from All Cancer Benefits in the Early Stages

- All tumors classified as benign, borderline malignant, or low malignant potential histologically

- Dysplasia, intraepithelial neoplasia, or squamous intraepithelial lesions

- Carcinoma in situ of the skin and Melanoma in situ.

- All tumors in the presence of HIV infection are excluded

All Major-Stage Cancer Benefits- Exclusions

The uncontrolled growth and spread of malignant cells, as well as the invasion and destruction of normal tissues, characterize this malignant tumor. This diagnosis must be backed up by histological evidence of malignancy. Leukemia, lymphoma, and sarcoma are all types of cancer. Benefits for major-stage cancer are not available in the case of the following.

# All tumors classified histologically as carcinoma in situ, benign, premalignant, borderline malignant, low malignant potential, neoplasm of unknown behavior, or non-invasive, including but not limited to Carcinoma in Situ of the Breasts, Cervical Dysplasia CIN-1, CIN-2, and CIN-3.

- Anynon – melanoma skin carcinoma until metastases to lymph nodes 4 or beyond are seen;

- Malignant melanoma that hasn’t invaded past the epidermis;

- All prostate cancers unless histologically classified as having a Gleason score greater than 6 or advanced to clinical TNM classification T2N0M0.

- All thyroid tumors with a histological classification of T1N0M0 or lower (TNM Classification);

- Less than Rai stage 3 chronic lymphocytic leukemia

- Non-invasive papillary cancer of the bladder with a histological classification of TaN0M0 or below.

- All Gastro-Intestinal Stromal Tumors histologically classified as T1N0M0(TNM Classification) or lower and with a mitotic count of less than or equal to 5/50HPFs;

- All cancers that are infected with HIV.

LIC Cancer Coverage Waiting Period (Plan 905)

A 180-day waiting period will apply from the date of policy issuance or the date of risk cover revival, whichever comes first, until the first diagnosis of “any stage” cancer. Any stage of cancer that occurs during the waiting period is referred to as “any stage.” This means that no money will be paid out under this policy, and the policy will be canceled if any stage of cancer is detected:

- Before the expiration of 180 days reckoned from the date of issuing of the Policy; or

- Before the expiry of 180 days reckoned from the Date of Revival.

LIC Cancer Coverage’s Survival Period (Plan 905)

If the Life Assured dies within 7 days of being diagnosed with any of the specified Early Stage Cancer or Major Stage Cancer, no benefit will be paid. The date of diagnosis is included in the 7-day survival span. The benefit under this plan will be paid if all of the following criteria are met:

- From the date of diagnosis, there is a 7-day survival span.

- Before death, cancer-related signs and symptoms should have been present and documented.

- All tests to confirm a cancer diagnosis should have been completed prior to the insured’s death.

- Satisfaction with the cancer definition as defined by the policy

Review OF LIC Cancer Cover (Plan 905)

- Customers can buy this package ONLINE, which is the best way to save money. You can save money by ordering it online (7 percent of Tabular Premium).

- The premium will be lower because this product functions similarly to traditional term life insurance, with no maturity benefit, surrender value, paid-up value, or loan value. Only if an event occurs (in this scenario, if you are diagnosed with cancer), will the insured receive a benefit.

- The benefits of detecting cancer at an advanced stage are far greater. Because you won’t have to pay any future premiums, you’ll just have to pay 1% of the applicable sum assured for the next ten years (irrespective of the term of the policy left).

- Every five years, the premium changes. As a result, unlike endowment or money-back plans, where the premium remains constant, the premium for this plan will change dependent on LIC’s claim experience. As a result, if the premium is no longer affordable after 5 years, you will be forced to purchase cancer coverage.

- A 180-day waiting period will apply. As a result, the risk will not begin immediately once the policy is purchased.

- This policy has a 7-day survival period as well.

- Even if your amount assured will increase by 10% each year, such an increase is limited to “the first five years beginning with the first policy anniversary or until the diagnosis of the first event of Cancer, whichever comes first” in the case of increasing sum assured. As a result, it will not be beneficial to you in the long run. After 5 years, you must purchase another similar coverage to cover the cost of cancer treatment at that time.

- It’s similar to term life insurance, but it’s disease-specific. As a result, if you do not have cancer within the policy period, you will not be eligible for any policy advantages such as traditional endowment or money-back plans.

- There is no TPA in this case. As a result, the claim may be a little complicated, and it often depends on how the concerned official handles it.

- Sec.80D provides tax benefits, but Sec.80C does not.

- General insurance providers offer a variety of cancer-specific insurance plans. I’m not sure why LIC was included in this category.

- The exclusions are difficult to comprehend for the average person. As a result, it is difficult for the average person to feel relieved that they are cancer-free.

- You cannot purchase it for your family as ordinary insurers do. You must purchase each item separately. This may result in the need to manage various plans, as well as an increase in costs.

- The Corporation will only pay one benefit if more than one Cancer is detected in an event. The amount pertaining to the stage of cancer with the highest benefit amount will be that benefit. This, too, I believe is a deterrent to this product.

- Furthermore, only ONE claim for early-stage cancer can be made during the insurance period.